How do we choose which fund managers to invest in?

Sep 06 2021 · 5 minute read

I have been struck by the coverage of the Tariq Fancy’s defrocking of the ESG industry. Without a trace of irony, he suggests that ESG as it is currently practiced by the asset management industry will lead us all into a false sense of security and will not address the environmental and social challenges flooding into our world. This is no great revelation as we look around the world and see the gargantuan problems that we are faced with — yes, clearly finance as it is currently practiced is part of the problem. The monitoring metrics that have so consumed ESG providers have shown themselves to be poor predictors of the outcomes we are seeking to achieve.

So, reshaping finance has become an imperative and Tariq is joining those of us who recognize that the short-term pursuit of profit, externalizing and outsourcing the long-term costs has run its course. Moreover, focussing on whether ESG funds outperform or not seems to be fiddling while Rome burns when what is required is a declared and monitored intention by asset owners to have a net positive impact and require their investments to do this.

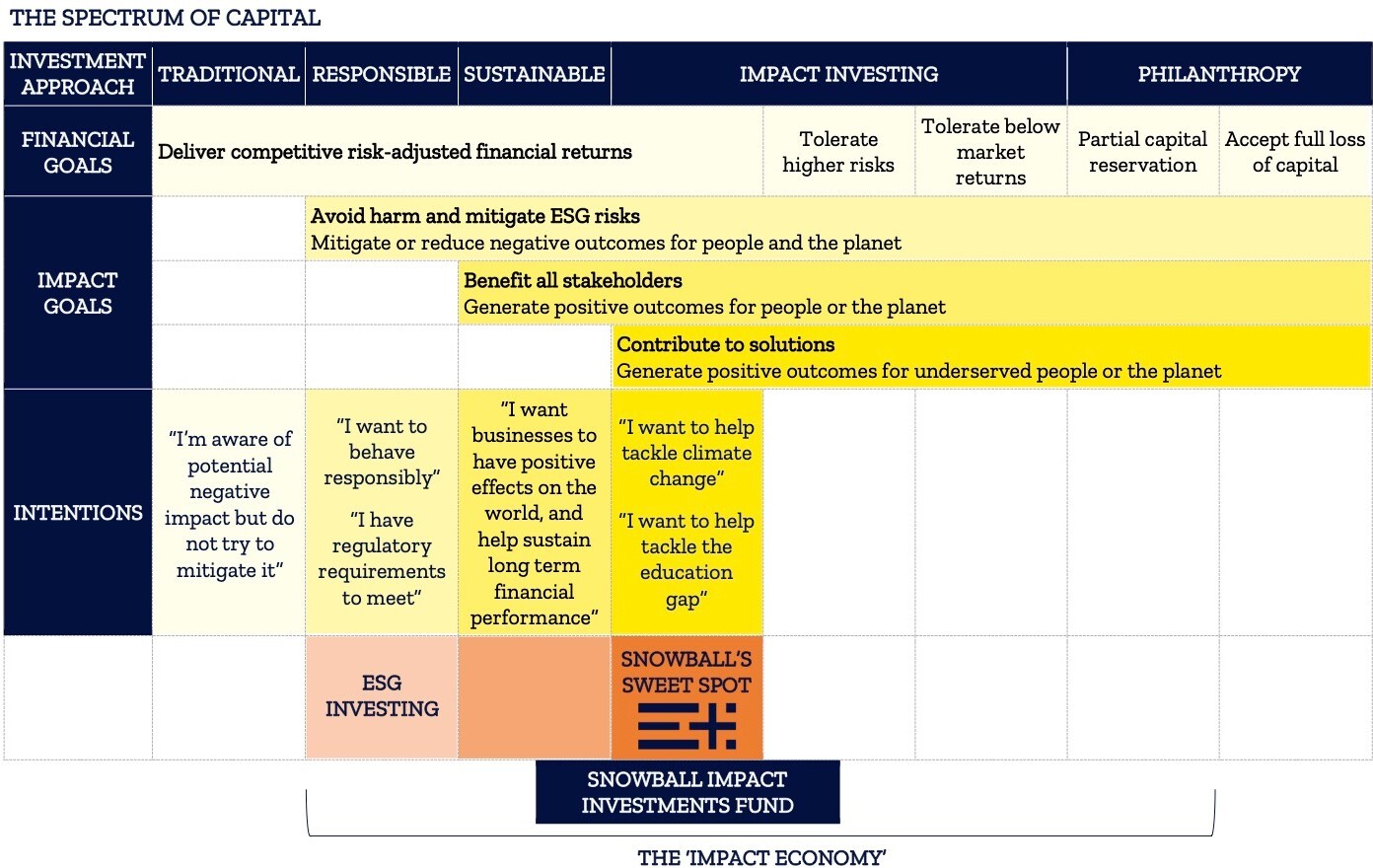

And there are fund managers out there that aim to do this — currently we are in the minority — but impact investing is moving apace, and the logic has become inescapable. As a fund of fund investor, we select fund managers that want to have an impact with their investments AND deliver a market return. Clearly not all impact investing can deliver market returns — nor should it — it is a broad spectrum. Snowball is investing in a sweet spot that is seeing a growing number of opportunities.

When selecting managers, Snowball uses a due diligence framework that digs deep below marketing spin and glossy impact reports. Here are our top 3 themes from that framework.

1. Mission and Behaviours

One of the key areas that Snowball looks at in a fund manager is its mission and behaviours. This assesses whether impact really drives an organisation and what systems are in place to ensure it delivers against this. Managers that score well on this tend to have a high percentage of assets under management in impact funds with senior management convincingly leading on impact. This means we end up with a higher proportion of focussed, boutique managers in our portfolio — names you may not be familiar with — and very few big shops. We really like fund managers that are B Corporations. They have a governance protected commitment to consider the impact of their decisions on their workers, customers, suppliers, community, and the environment — about 25% of our assets are run by B Corporations.

Managers also may have elected to tie some of their own financial returns to the impact that they generate — typically we see this in the private equity space where impact is tied to the carry a manager can take once a financial hurdle has been achieved. But impact measurement is difficult to do well and whilst we would like to see more of these approaches, we are wary of GIGO (garbage in, garbage out) and the false promises that Tariq Fancy also warns of.

This brings me to another area of focus that we recommend in due diligence — an analysis of the impact approach that a fund manager is using.

2. Impact Approach

Fortunately, the non-profit sector has led the way on showing us the importance of focussing on outcomes and creating a theory of change which can deliver to those outcomes. In our portfolio, we have a public equity manager that creates a theory of change for each investment, tracking KPIs tied to the outcome targeted. Another manager, investing directly in private companies, produces a stand-alone theory of change report which is refined and challenged throughout the lengthy and detailed private market diligence process. Both managers are generating excellent financial returns alongside a deep and genuine commitment to understanding and improving the impact of their portfolio. Impact measurement at its best should provide inputs into business decision making — so asking businesses to provide impact metrics that don’t help them run their business is a waste of everyone’s time and leads to the meaningless footprint data that frequents some impact reports.

And so, to the final (deceptively simple but very powerful) element of a robust impact due diligence process — actually reading impact reports! Bizarre but true.

3. Read the Reports

By reading these reports, we are trying to

understand if the manager is trying to make a real-world improvement through the way they invest.

Is the report open about challenges and failures

or is it merely a marketing document? We like to

see reporting on impact data, against a recognised

framework, over time — so we can see what the

trends are.

We report back to managers about what we have learned by reading their report, and discuss with them where we think they can make improvements.

Through doing this we get a deeper understanding

of the intentionality of a manager in investing for

impact. We build long term relationships with fund

managers and make more informed investment

decisions. And we build a portfolio that optimises

for impact whilst delivering a market return.

If you have any thoughts about this article or would like to learn more about Snowball, please email us at hello@snowball.im.