Not an ESG investment.

Jan 24 2022 · 10 minute read

This article was published in Philanthropy Impact magazine, Issue 26, Winter Edition. You can download the a full copy of the magazine by visiting the Philanthropy Impact website: https://www.philanthropy-impac... . Philanthropy Impact is a non profit organisation providing learning, resources and analysis to impact investors, philanthropists and their advisors.

JOURNEY TO A FUTURE WHERE ALL INVESTMENT WILL CREATE A POSITIVE IMPACT FOR SOCIETY AND OUR PLANET: A CASE HISTORY

I approached impact investment from the perspective of a grant-giving philanthropist at the Golden Bottle Trust, which is the C. Hoare & Co charitable foundation. Whilst we had succeeded in making some systemic and catalytic grants, I felt that many grants were not achieving very much.

In 2010, the trustees empowered me to make social investments of up to 10 per cent of the endowment, and quite quickly afterwards they were encouraged enough to raise the limit to 20 per cent. The first investment was in equity, the second was in the pioneering Peterborough Prison Social Impact Bond, and then I found that at that time it was possible to earn 5 per cent on debt (loans to charities) whereas the bank was paying little or nothing on deposits, so we invested in some debt instruments (including a microfinance fund).

Within a few years, we had our first clear lesson: this was not a part-time activity but required both in-depth investment and impact measurement expertise. This finding prompted us, in 2015, to join up with another non-profit, Panahpur, which had committed to invest 100 per cent of its endowment into impact solutions. Together, we hired the professional team we needed to expand what we were doing, and to deliver our big ambitions to encourage others to invest in this way — and created Snowball. We were quickly joined by Friends Provident Foundation, Skagen Conscience Capital, Gower Street, and the Ian Taylor Foundation, who all wanted to align their assets with their missions. At the time, these partners had to take all investment decisions as the partnership was unregulated.

TACKLING THE SDGS

We built an investment portfolio whose capital contributed to tackling all 17 United Nation’s Sustainable Development Goals (SDGs) intentionally and additionally. These goals will never be met with just philanthropic and taxpayer’s money — it was and still is important to mobilise mainstream investment markets.

We wanted to keep the impact themes broad, and to demonstrate that it is possible to achieve competitive returns and measurable impact. The portfolio used cash and fxed income, public equities and private equities, and some venture fnance. Importantly, the fund was designed to be evergreen (which is to say that we do not have to liquidate investments and wind up the fund at any particular time).

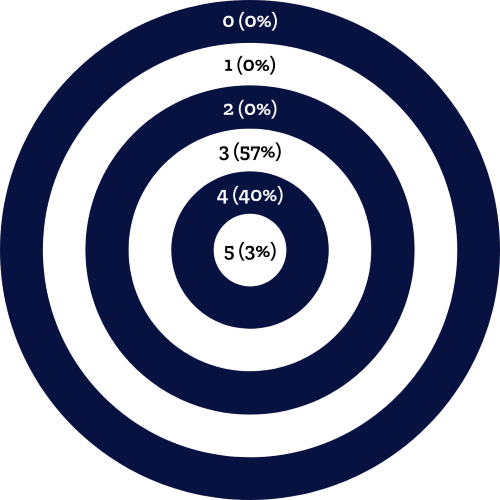

We were early members of the Impact Measurement Project — we adopted their methodology in order to contribute to a coalescing of standards, but we also added to their thinking in the way it can be applied in a multi-manager or “fund of funds” context. Part of this work involved designing an impact framework, and a simple visual to display the impact score of portfolio holdings and of the portfolio as a whole. This is our “bullseye”. We later won two awards for the impact management methodology we developed (Pensions for Purpose, 2019, Impact Strategy Award and Most Read Content for the first report we published on it).

SNOWBALL IMPACT METHODOLOGY

The bullseye chart denotes the impact intensity of our portfolio by showing the % of the portfolio that sits in each ring of the bullseye. We aim to drive the impact score toward the centre of the bullseye.

Having started to establish our track record delivering good financial returns and measurable impact, we wanted to review our structure and how it would support our momentum towards our overall mission. The difficulty with this form of partnership is that it is difficult to scale, as not all prospective investors want to sit as full partners, preferring to delegate to expert and active investment management, optimising for risk, return and impact. So, in 2019, Snowball was re-born as a conventional GP/ LP-regulated fund with a much lower entry ticket (£150k). This was a key intermediate step in our journey towards making it possible for everyone to invest in solutions to improve society.

One merit of a familiar structure is that it is easier to compare with other such investments. We contend that an impact investment portfolio offers good risk-adjusted returns. The returns are lower than you can obtain in focused and leveraged funds, but our fund is very diverse across geographies and sectors and is not leveraged. Also, our fund held as part of any conventional portfolio should improve risk adjusted returns by diversifying exposures in the portfolio. Snowball delivered 7 per cent in the first six months of 2021, well ahead of our target of 6 per cent per annum. Markets have benefited from much central bank support over the past 15 years — the true test of our conviction will be in next market correction, and we expect the value of holdings contributing to solutions to social issues to fare better than pure financial investments.

Snowball holds newly invested cash in public equities whilst awaiting the next private impact fund to close so we deploy quickly into impact. These are shares that would hold their own in mainstream investment markets, maximizing returns for a given level of risk, using ESG measurement metrics.

NOT AN ESG INVESTMENT

Snowball, however, is not an ESG investment: instead, our requirement is that the funds we invest in are invested in companies whose products and services create a measurable and additional positive social outcome.

This means that the bulk of our investments are in instruments to which the conventional mainstream markets would not allocate (or not until very recently). Examples include Resonance social housing, including their Women in Safe Homes Fund; Circularity Capital; and The Yield Lab. These are intentional and measurable impact investments, and they differ from ordinary financial investments with an ESG label, or who are scoring ESG risk. The problems with ESG investing are being intensely discussed, with Tariq Fancy, Desiree Fixler and James Anderson sharing insider views to accelerate a much needed focus on integrity and standards. Elsewhere, industry observers like Columbia Business School are highlighting the way that self-proclaimed ESG companies and funds are falling well short on their commitments. Reshaping finance has become an imperative and these ESG escapees have joined those of us who recognise that the short-term pursuit of profit whilst externalising and outsourcing the long term costs of that profit has run its course. Snowball is completely changing how we all think about investing. We are pioneering new ground as much as possible, being transparent and sharing our learning as we go. Our theory of change will be achieved by a systemic transformation of financial markets.

FOCUS ON PURPOSE

According to the Global Impact Investing Network, the global impact investing market is $715 billion. Big Society Capital size the UK market at £6.4 billion, and their new strategy is to double it in five years. We think this is more than achievable. The pandemic and dramatically heightened awareness of the environmental crisis running up to COP26 (among other things) have prompted people to think about the purpose of their investments. The difficulty is that there is a gulf between thinking we can do better and putting our money to work in a new paradigm.

So far investors and families that consider society alongside profit have been in the vanguard. There are trustees of many foundations and charities who would like to invest in line with their purposes, but they have been outnumbered by more conservative colleagues wedded to the status quo. Most wealth managers are aware that the next generation would like to see at least some impact investing in their portfolios, but in general they focus on comparative performance (and their bonuses). And so progress is slow, but it is also sure. Snowball is gratified recently to have won new mandates from foundations like Bridge House Estates and the EIRIS Foundation, as well as from individuals and family offices. We hope this public recognition will convince some of those who have been watching and waiting that it is OK to change with the times.

Putting the money to work appears to be less of a challenge. More and more entrepreneurial funds that tackle a broad range of social problems both in the UK and globally are crossing our desks.

At the next close (which is the end of November 2021) the fund is set to be twice the size it was 18 months ago. We are speaking with potential cornerstone investors to increase our momentum whilst continuing to welcome new individuals, families and charities to invest with us. Our goal is to grow our investor base to the point at which we will be able to allow more people to access the intentional, measurable and additional impact investments we are making. An important benefit of investing through Snowball is that it gives individuals access to private equity holdings they could never obtain on their own unless they were seriously rich.

Returning to the Golden Bottle Trust where I started, it is pleasing to report that the endowment (~£19m) is 100 per cent invested for impact across four fund managers and some proprietary investments, and the performance has been very satisfactory for the charity. Our giving has also been fruitful, and an impact report can be found on the Hoares Bank website.

SNOWBALL PORTFOLIO: FUND SPOTLIGHT ANANDA IMPACT FUNDS I & IV | PRIVATE EQUITY SDGs 3, 4, 8 & 10

Founded in 2010, Ananda Impact Ventures was an early pioneer in impact venture capital.

The manager’s strategy is to invest in, and scale, impact driven for-profit enterprises across healthcare, education, sustainability & social justice. Snowball is invested in Ananda’s first fund and has committed to the fourth fund.

Ananda invests in companies which are reaching underserved groups. The majority are explicitly committed to reaching vulnerable populations, such as children from a disadvantaged background (e.g. Third Space Learning, a one-on-one online numeracy tutoring programme for children on the Pupil Premium), older people (Careship, an affordable live-in care provider for elderly patients); and people with disabilities (e.g. Auticon, an IT consulting firm which provides employment for people with autism).

Ananda meets Snowball’s financial return requirement for impact venture and growth equity. Impact is at the core of its operations; all its assets are invested for impact. Snowball believes that Ananda walks the walk when it comes to impact – for example, the manager’s carry is tied to impact, it has an impact term sheet which is genuinely pioneering and an independent advisory committee which signs of on KPIs and targets.

SNOWBALL PORTFOLIO: FUND SPOTLIGHT AQUA-SPARK | PRIVATE EQUITY | ENVIRONMENTAL SUSTAINABILITY | SDG 14 | c. €150 AUM (OPEN-ENDED FUND)

Snowball invested in Aqua-Spark

in January 2021.

Aqua-Spark is a Dutch co-operative, launched in 2014, which invests in sustainable aquaculture businesses with a mission to move the aquaculture industry towards healthy, sustainable and affordable production. It will invest in 60-80 companies across the aquaculture value chain (eg. alternative feed ingredients, farming operations, health and disease prevention and farm management technology) to achieve wider systems change.

Example companies in its portfolio are Calysta (which turns methane gas into a protein which can be used in fishmeal), Sogn Aqua (a land-based Atlantic Halibut farm which showcases best aquaculture practices – eg. feed conversion ratio below 1:1, all materials are recyclable, humane practices, no chemicals or antibiotics, systems designed to replace nature and hydro powered) and Proteon Pharmaceuticals (which provides animal health solutions using bacteriophages, a healthy, natural alternative to antibiotics).

Snowball chose to invest in a mission-aligned manager achieving impact alongside a bolder ambition to change the aquaculture industry, whilst also addressing our limited portfolio exposure to SDG 14 (Life Under Water). As an open-ended fund, Snowball intends to scale this investment as they grow.

ALEXANDER HOARE – PARTNER AND DIRECTOR, C. HOARE & CO.

Alexander is the first of the eleventh generation of Hoare family members to run the bank. A graduate of the University of Edinburgh (B. Com (Hons) Marketing), he joined the bank in 1987 from PA Consulting Group where he worked as a Marketing Consultant. From 2001 to 2009, he was CEO of C. Hoare & Co.

Alexander is a leader in the field of impact investing, and a Founder Partner of Snowball. He serves as President of the Groupement Européen de Banques; as a Patron of Royal Trinity Hospice; and as Chairman of the Trustees of Intermission Youth Theatre.

If you have any thoughts on the article or would like to learn more about Snowball, please do be in touch on hello@snowball.im